Archived Insight | January 31, 2019

Equity Markets in 2018: Reflecting on a Volatile Year

- Volatility returned to world equity markets in 2018, causing turbulence in stock performance throughout the year.

- Some markets experienced the largest annual declines since the global financial crisis of 2008.

- Times like these are a reminder that equity investing is a long-term commitment, which involves riding out the downturns in order to capitalize on the upside.

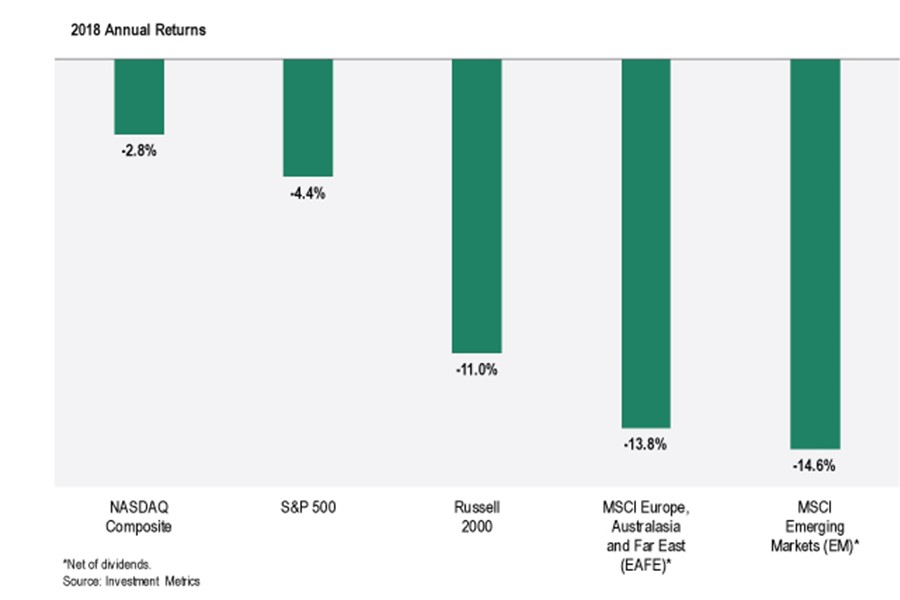

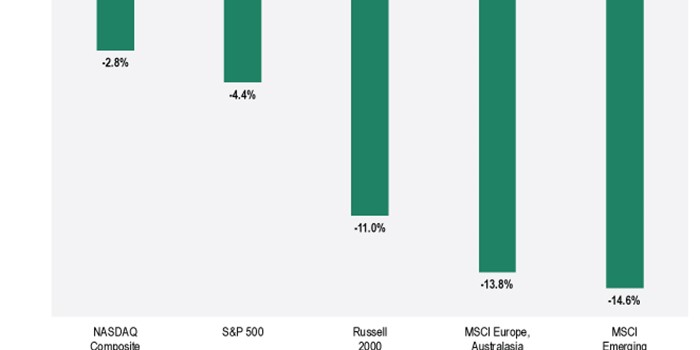

Coming off strong double-digit annual returns in 2017, equity markets in 2018 looked much different.

In the U.S., volatility returned in February after more than a year of being in hiding, in a reaction to what should have been positive news about the U.S. economy spurring fears of rising inflation and interest rates.

In March, trade concerns began, with the U.S. implementing tariffs on imported goods and the response in kind by some of our biggest trading partners.

After a summer of climbing the classic wall of worry, October arrived, bringing with it the third rate hike this year from the Federal Reserve (Fed) and strong employment gains, foreshadowing further rate increases and sinking the equity market once again.

Stocks rebounded a bit and ended November in positive territory, but another slide started later that month and carried over into the worst December for U.S. equities since 1931 and ultimately the largest annual decline since the global financial crisis.

Outside of the U.S., equity markets also fell, with a rising U.S. dollar, slowing economic growth and concerns about global trade weighing heavily on stocks around the world.

While U.S. equities took a hit in 2018, non-U.S. markets experienced even steeper declines, as shown in the graph below.

Is This the End of the Bull Market?

While it is said that bull markets don’t generally die from exhaustion, this one is looking pretty tired. The reaction, consistent with the environment of a latish cycle period, to any sort of news has generally been “Oh, this must be bad.”

The Fed raising rates again in December (as it had previously indicated it would do) and saying it plans to increase rates three times in 2019 was good news, which should have translated to, “We see the economy continuing to grow nicely and want to make sure that it doesn’t overheat,” but instead it was interpreted as bad news.

The Fed subsequently revised its statement to say it would raise rates in December and maybe twice in 2019 depending on what happens, which was mixed news, but was also perceived as bad news.

A limited government shutdown is bad news, an unknown Brexit is bad news, trade tiffs are bad news, and the roll-off of tax cuts is bad news.

The sun coming up may as well be bad news. Interestingly, though, almost all of the news shares one common element – it is old news.

The big question is, “So what’s next?” And the answer requires an answer to another question – “When?”

If it is next month – no one knows. If it is next year, what Segal Marco Advisors is hearing from the people we are talking to (and that is a bunch of folks who are not just coming in off the streets) is fairly universally that a bear market is not anticipated, but it’s not looking like a bull either.

In the near term, equity returns are generally expected to be modest as the various issues are absorbed or resolved in the future. Some lean a little more towards the low single digits and some foresee higher single digits, with the latter convinced that things being cheaper now will contribute to better results.

If the timeframe is the next 10 years, then we continue to believe that equity markets will provide an attractive opportunity for investors, with the inevitable bumps and bruises along the way (see the next section below).

Given the widely held belief that growth in the developed world will be relatively muted due to modest increases in GDP, we anticipate that those equity markets will see returns that average more in the 6.5% to 7.5% range. But, with inflation in the low single digits, the real returns, while not exciting, should be within an acceptable level relative to long-term expectations.

What Goes Up Comes Down, and Goes Back Up Again

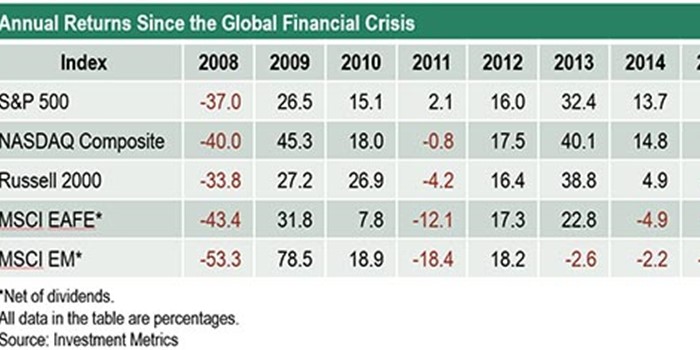

Looking back on the history of the markets since the 2008 crash in the table below, we can see the fluctuations in annual returns.

Using U.S. small caps as an example, we see a significant rebound in the Russell 2000 index from 2008 to 2009 and 2010, followed by a decline in 2011, a subsequent strong gain in 2012 and 2013, a modest return in 2014, a fall in 2015, and a seemingly repeating pattern in the years following.

What this example shows us is that market swings are normal. While equities have lost ground this year relative to the last two years, history says they will come back up.

Times like these are a reminder that equity investing is a long-term commitment, which involves riding out the downturns in order to capitalize on the upside. Investing in the markets always carries risks.

Having discipline, rebalancing, reviewing policy allocations, diversifying portfolios, monitoring cash flows, and other consistent best practices help protect investors amid volatility or market declines.

Segal Marco Advisors provides consulting advice on asset allocation, investment strategy, manager searches, performance measurement and related issues. The information and opinions herein provided by third parties have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed. Segal Marco Advisors’ R2 Blog and the data and analysis herein is intended for general education only and not as investment advice. It is not intended for use as a basis for investment decisions, nor should it be construed as advice designed to meet the needs of any particular investor. Please contact Segal Marco Advisors or another qualified investment professional for advice regarding the evaluation of any specific information, opinion, advice, or other content. Of course, on all matters involving legal interpretations and regulatory issues, investors should consult legal counsel.

The information and opinions herein provided by third parties have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed. This article and the data and analysis herein is intended for general education only and not as investment advice. It is not intended for use as a basis for investment decisions, nor should it be construed as advice designed to meet the needs of any particular investor. On all matters involving legal interpretations and regulatory issues, investors should consult legal counsel.