In 2020, SPACs became a force that overwhelmed the IPO market. SPACs are not a new phenomenon, but the unique characteristics of these vehicles may have been identified as more suitable for prevailing markets, thus leading to their re-emergence in dramatic fashion. While there may be no one specific reason, the COVID-19 outbreak, subsequent market and economic turmoil could all have simply been the collective impetus that ignited investor interest.

Key points

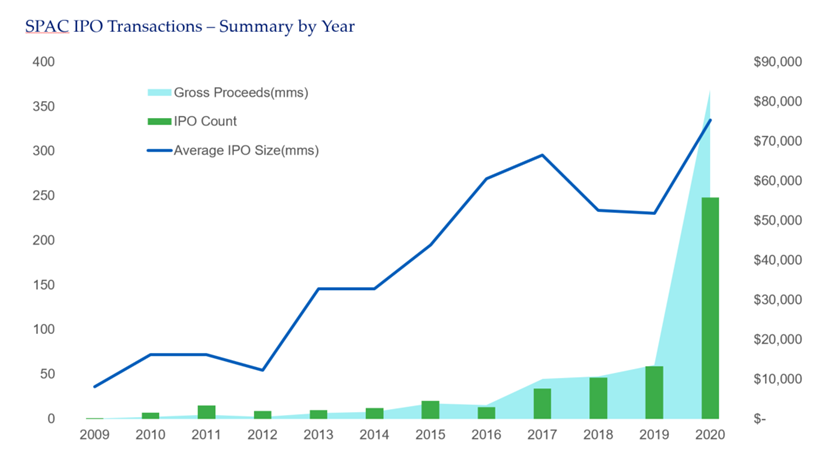

- Over 200 SPACs were launched in 2020, over 3x in count & over 5x in gross proceeds year over year, respectively

- For 2020, SPACs have accounted for more than 40 percent of the money raised in IPOs; of which 53 percent was raised in the last four months of 2020 alone

- SPACs have only averaged roughly nine percent of money raised in IPOs, marking more than 4x growth in SPACs in 2020

- Total SPAC capital raised in 2020 ($83B) also exceeded totals raised over the entire trailing 10 years ($47.1B)

- At the market’s current rate, SPACs will have a ratio of 5x equity capital to target merger and acquisition (M&A) enterprise value (EV)

- Total EV of future SPAC acquisitions could lead to ~$300B in M&A activity over the next 12-36 months (range based on the typical 24-month period allotted to SPAC sponsors to execute acquisition)

- This figure is significant but is dwarfed by the $6T+ of assets held by private market funds globally

- 2021 is already off to a strong start, with nearly the same number of SPACs listing (53) as in 2019 (59) and with more gross proceeds ($14.7B) than 2019 ($13.6B) as well

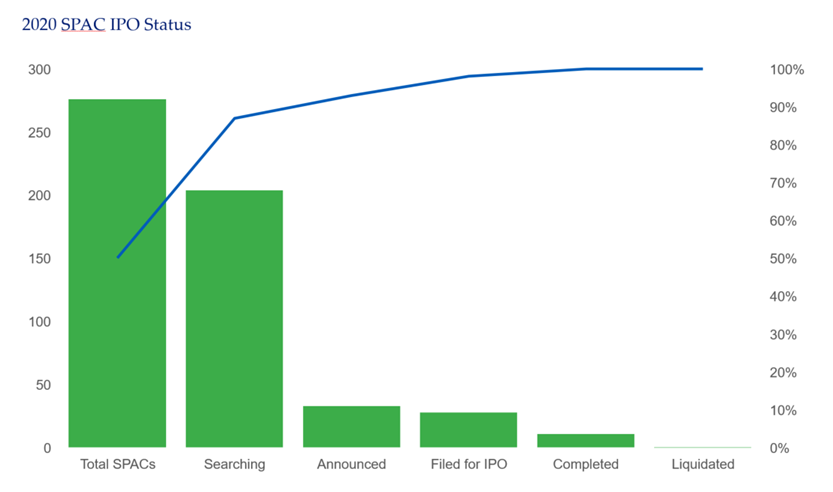

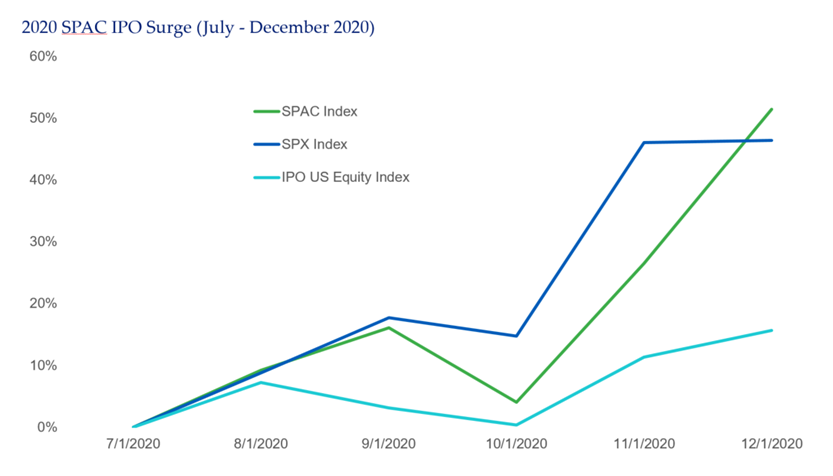

2020 SPAC Performance vs. S&P 500 & Renaissance IPO Index

What are SPACs?

A SPAC is a publicly listed holding company that raises capital to specifically acquire other companies. These are non-operating entities and often also act as investment vehicles that raise investor capital to make such investments. With a few exceptions, most SPACs list at $10 per unit (akin to a share) and only see a share price difference after an acquisition announcement and/or a deal closing. Unlike an investment fund, SPACs typically acquire a single portfolio company rather than construct a diversified portfolio of holdings.

SPACs, specifically, have most often been used as a listed investment vehicle that can acquire private companies to take over/reverse merge companies into the SPAC. (A reverse acquisition is when an existing public company – the SPAC – acquires a private company and operates it in a public company structure.) This nuance is the “back door access” to public markets (i.e., avoiding the potential high costs, time-consuming registration and road-show processes of IPOs) so often associated with SPAC-owned companies. SPACs have been used by private equity investors and private companies alike to obtain financing, liquidity and exit investments instead of the more traditional IPO process.

Generally, a SPAC is very similar to a private equity (PE) fund. Both are blind pool investment vehicles that raise capital from investors, attempting to identify and invest in companies with the goal of selling them at a higher value than initially purchased. PE funds are designed to invest in multiple companies whereas a SPAC is primarily meant to invest in a single platform company. Further, SPACs are typically required to make an acquisition at a fair market value of 80 percent or more of the SPAC’s available capital within a specified period. Unlike traditional PE funds, when a target company has been identified by a SPAC’s management team, they are often required to present the deal to the SPAC’s investors as they retain the right to forgo the investment and redeem their invested capital. Should no deals be executed in the defined timeframe, the SPAC is dissolved and capital returned to investor’s pro-rata plus accrued interest from its trust. The SPAC’s sponsor will forfeit their original investment.

The allure & issues related to SPACs

For private equity investors, SPACs offers another route to execute a buyout or venture investment with potentially less upfront equity, debt and fees associated with such transactions. Effectively the sponsor (manager of the SPAC) “commits” or invests two to five percent of their own capital.

However, instead of committing to their own PE fund, the sponsor is purchasing the “founder’s shares” of their own SPAC in its IPO. The difference with SPACs is that the sponsor invests in “founder’s units” (essentially shares) that include warrants typically providing a 20 percent ownership stake in the SPAC once an acquisition deal is completed.

Warrants associated with SPAC investments offer an attractive deal, enabling investors to increase ownership of a company, if a transaction is successful. For every unit owned by an investor in a SPAC, there is an attached warrant to purchase more stock at a later date.

While the sponsor’s commitment appears to be in their favor rather than their investors’, there are other terms of SPACs that provide investors more investor-friendly elements, such as redeeming capital. Unlike locked-up private equity funds, SPAC investors reserve the right to opt out of participating in a SPAC’s target acquisition and are granted the ability to redeem their investment accordingly.

The only loss is a time value of money matter, or opportunity cost, as the capital is deposited in a trust for the period. By doing so, this puts the SPAC at a possible disadvantage versus traditional private equity funds, as the sponsor could be preparing to close a deal only to have the capital base disappear pre-closing.

For private companies, SPACs present a third alternative to liquidity (IPO and direct listing being the other two) and access to public capital markets for future growth initiatives. Once a SPAC completes its reverse acquisition, the private company acquired can reap the benefits of a public company while also assuming the less desirable characteristics.

Through a SPAC, acquired companies benefit from being publicly traded and the improved investor awareness that comes with this listing. Further, companies can improve their access to capital vis-à-vis public markets, including easier equity financing for M&A, ownership liquidity, and public debt markets. SPAC-listed companies also bear the regulatory burden. Examples include the increased reporting requirements and their associated costs mandated by the SEC and other regulatory bodies. This regulatory compliance feature is a widely stated reason why companies prefer to remain private and why SPACs can be preferred to IPOs, however, there is some evidence showing that the regulatory cost burdens have come down in recent years.

From an underwriting and due diligence perspective, SPACs provide further benefits to investors. The typical reverse merger process permits companies to provide SPAC shareholders with revenue, earnings, profit and growth projections of the targeted acquisition, which is prohibited in IPO listing processes.

From the view of a target company, SPACs permit companies to raise new capital during this process, whereas IPOs prohibit priced financing rounds during their transition process. Direct listings have recently been amended by the NYSE to permit financing activities, but historically had been prohibited.

Regardless, the improved transparency into a company’s financials and its own projections can lead to more customized structuring, relative to the traditional IPO. Flexibility provided by SPAC acquisitions can be mutually beneficial. Many believe sponsors have a greater chance of favorable purchase prices that more fairly represent a company’s current intrinsic value.

For the company, SPAC’s provide benefits including the option to raise more capital on a relative basis by increasing equity issuance through a private investment in public equity (PIPE) or by the SPAC itself. In addition, SPACs have included more private equity-like characteristics such as earn-outs for executives of the acquired company based on achievement of certain business performance objectives and favorable shorter duration lock-ups.

In this framework, SPACs present a more direct and potentially less costly, risky and more certain conduit to public capital markets. In roughly reverse order from an IPO, companies engaged in a SPAC financing agree to sell to a single investor at a predetermined valuation and share price that is then announced during or simultaneously with the closing.

The potential risk mitigation includes: (i) no adverse press if the deals fails potentially hurting the perceived value of the company; (ii) greater valuation clarity versus a more typical 1+-year IPO road show testing prices a huge number of potential investors may be willing to pay; and (iii) no potential impact from public market investors’ shifting sentiments while trying to live up to or justify post-IPO valuation highs experienced in recent bull market. This is particularly advantageous for companies in the tech, healthcare and lifescience/biotech sectors that have inherently complex services sold and relatively longer paths to profitability given the required development needs.

Distinguishing characteristics of SPACs

SPACs and private equity funds (specifically buyout funds) share very similar mandates; they both seek to make control-equity investments in companies in which they want to be a majority owner. Where things differ is more on the side of the company looking to sell or complete a financing round.

Furthermore, there is greater implication to the venture capital markets and those companies backed by venture funds. The traditional IPO exit route provides the promise for significant upside in valuation and a liquidity event for both the venture capitalists (VCs) and employees of the company. With IPOs, founders and existing management team members typically retain both controlling equity and voting rights of their companies. Once public, the founders and other owners maintain control and manage ongoing business plans.

On the flip side, while SPACs do provide the requisite liquidity and promise of upside, both are potentially muted at first relative to IPOs. Unlike IPOs, SPACs typically involve a single investor for companies to deal with, truncating the process and mitigating what can be an arduous IPO process. Simplicity, speed, and efficiency in closing with a single, long-term oriented investor will always be preferred by companies, but those advantages do not come for free. The cost is typically a lower purchase price valuation, but this could also lead to more efficient and effective price discovery with potentially less future pricing volatility, without the whims of potentially tens of thousands of shareholders, such as with IPOs. In this framework, it makes sense why SPACs came back in such dramatic fashion in 2020. It was a risk-taking and transfer exercise where public markets and IPOs were offering no liquidity or appetite, but the need for capital access did not subside. For companies, SPACs meant they could raise their requisite capital needs but only from an investor willing to take on such risk in a bad environment. In doing so, the company takes a haircut on their share price in order to improve the certainty of closing.

The fact that SPACs are synthetic buyout funds seeking control of companies may present an issue to companies contemplating SPACs alongside direct listing or an IPO as a potential financing and/or public market liquidity option. More specifically, this could be a hurdle for those companies that are VC-backed and/or where founders want to continue acting in executive management roles. Once a SPAC deal is done, the SPAC’s management team is now the majority and controlling equity owner that will ultimately manage the company on a go-forward basis. VCs and founders alike may be apprehensive about turning the keys over simply to avoid the IPO or direct listing processes.

To circumvent both the universe of investment opportunities and certainty of closing success, an increasing number of SPACs are being launched and managed by alternative investment managers themselves, using their own funds’ portfolio companies as investment targets. While there is nothing inherently wrong with a ready-made and available pipeline of companies with relatively assured closing potential, this narrow scope of assessment by nature introduces a high degree of bias in investment selection. And in such cases, the individuals managing these funds stand to benefit from both the monetary reward for realizing an exit in their PE fund while simultaneously being granted their 20 percent promotion in the SPAC from just doing the deal.

The future of SPACs

The structure and inherent features of SPACs present attractive solutions for companies in need of further financing or looking for liquidity. Companies have a need and investors have a desire to allocate capital to potentially high-growth tech and healthcare companies that could give them the returns they want. Timing and prevailing market conditions seemed right to dust off the SPAC structure and it quickly became an attractive vehicle to execute such investments during a time when there were little to no options.

For specific sectors and long, long-term growth stories that require patient long-term capital, SPACs could find a more permanent home where acquisition-based ownership, familiarity with SPAC sponsor’s ability to create value, and potentially more stable valuation could make SPACs a prudent alternative to IPOs. While it is far too early to tell whether SPACs will remain a primary tool for public market access, the potential scalability of and ownership structure of SPACs may prove to be a limiting factor.

For allocators, SPACs present an attractive opportunity to invest capital in potentially high-growth companies in a more liquid and potentially less volatile manner. Since they typically take two years to invest in a company, SPACs provides the advantage of patience while providing an opportunity to exploit market inefficiencies arising from bouts of volatility and the capital needs of private companies with few other alternatives.

The 2020 SPAC phenomenon has seen a large number of investment options that are not all created equal. There will be some standout winners; however, the potential reward will be met with, at a minimum, commensurate risk and losers.

Works Cited

- DealLogic

- McKinsey & Company

- Goldman Sachs, Bloomberg

- Goldman Sachs

- Seward & Kissel

- Renaissance Capital

- Pitchbook

- SPACinsider

- SPACdata.com

See more insights

The information and opinions herein provided by third parties have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed. This article and the data and analysis herein is intended for general education only and not as investment advice. It is not intended for use as a basis for investment decisions, nor should it be construed as advice designed to meet the needs of any particular investor. On all matters involving legal interpretations and regulatory issues, investors should consult legal counsel.