In 2022, one of the foremost concerns for investors (as well as consumers) is inflation.

In this article, we consider inflation as it relates to your investment program. We address these key questions:

- How should you be thinking about inflation?

- Should inflation risk be hedged?

- If so, how?

Today’s inflation rate in perspective

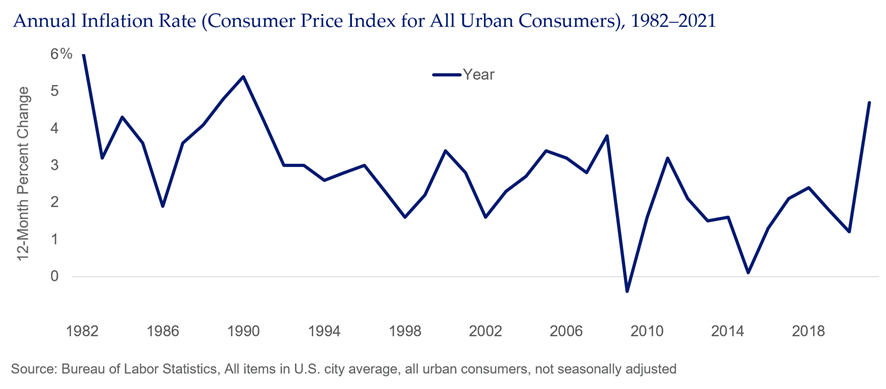

2021 saw inflation rise to levels last seen almost 40 years ago, as illustrated in the graph below. Consequently, many people have not felt the bite of endemic inflation on their wallets or their portfolios.

We began 2021 with the U.S. Federal Reserve (the Fed) calling inflation “transitory.” (We discussed whether inflation is transitory in our article, “Did Big Ben Answer the Question?”) The year ended with the Fed removing the word “transitory” from its guidance. Clearly, we have entered, at minimum, an inflationary environment, with the question being duration.

Up to this point, as is often the case, inflation has provided some benefits, most directly in rising wages (and increased consumption of goods as a result). But, looking ahead, if we reach inflation that is persistent, will we see more negative effects? If so, how should an investor think about the risk of inflation on a portfolio?

Inflation is in the eye of the beholder

Inflation risk impacts a portfolio differently depending on the cohort.

As an individual, I care that prices are going up. What I buy today — be it food, gas or clothing — all now put a bigger dent in my wallet. The severity of the impact to individuals is related to wages and disposable income. Retirees, given their fixed income, will feel inflation’s bite particularly hard.

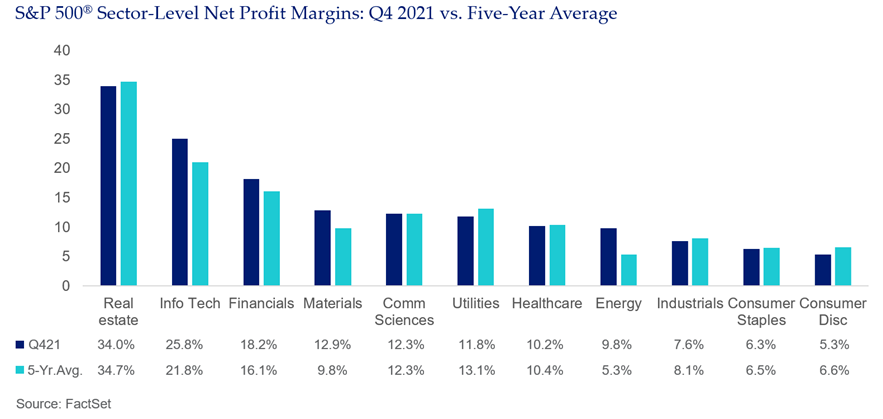

For corporations, the impact will be felt most directly as input costs rising. But, ultimately, the pain will depend on how much of the increase in prices can be passed on to the consumer. (As an aside, in 2021, given that margins were very positive, one can conclude much of the cost increases have been passed on to consumers).

If, however, a corporation cannot pass on price increases, margins will suffer. If margins suffer, valuations may begin to suffer and will be reflected in declines in the equity market.

The S&P 500® Index is a product of S&P Dow Jones Indices, LLC and/or its affiliates (collectively, “S&P Dow Jones”) and has been licensed for use by Segal Marco Advisors. ©2023 S&P Dow Jones Indices, LLC a division of S&P Global Inc. and/or its affiliates. All rights reserved. Please see www.spdji.com for additional information about trademarks and limitations of liability.

In the investment management world, the impact of inflation on an investment program will be both direct and indirect. For example, public sector funds often have built-in cost of living adjustments, so 2021 will directly impact the cost of benefits. Corporate pension plans have an actuarial wage assumption, which will be felt, albeit slowly, as inflation impacts wages. Inflation will have a direct impact on endowments and foundations where spending formulas are generally based on inflation. Multiemployer plans’ benefit costs are related to contracts and collective bargaining. Real wage increases, if bargained, will mitigate the impact of inflation on real spending (thus impacting the cost of corporations delivering products and so the inflation circle turns).

Hedging inflation risk

In all of the cases mentioned, the level of inflation, and in particular, its duration, is a risk to consider. Just like all other investment program risk, such as interest rate risk or market risk, investors should review current inflation risk.

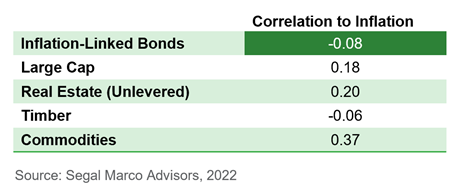

Generally, a well-diversified investment program will have some embedded inflation hedging characteristics in the investment portfolio. Equities, real estate and other real assets, as well as Treasury Inflation-Protected Securities (TIPS) all have some built-in inflation protection.

- Equities are often thought of as having inflation protection, and 2021 was an example of this. However, the degree of protection depends on the inflation regime. If it is demand inflation, such as what we experienced in 2021, companies can pass through increased costs by increasing prices and protecting margins and, thus, earnings and valuations. Conversely, inflation that is long in duration (persistent) or high (some research suggests 8 percent is the level) will reduce growth and real economic activity, which in turn will negatively affect the market. Finally, when discussing equities, there are many sectors and types of equities, which will have varying responses throughout an inflationary environment. For example, during the '70s inflation era, oil prices surged due to supply issues and oil-related stocks outperformed other sectors of the equity market.

- Real Assets, such as real estate, timberland, agriculture and infrastructure, are all investments that can provide protection against inflation to varying degrees. Real estate is interesting in that while some aspects of it provide protection against inflation (i.e., higher income through increasing rates), multi-family and single-family real estate are also direct contributors to inflation metrics through the shelter components of the index. (We discussed this in our article, “Define ‘Inflation’ for Me. It’s Harder Than You Think.”) Shelter contributes 40 percent of the weight of the core consumer price index less food and energy (CPI-U) and one-third of the basket for the inflation index (CPI).

- TIPS can offer the most direct protection against rising inflation. However, TIPS returns are also impacted by changes in interest rates. Given the current expectation is for a rising rate environment, the duration of the TIPS portfolio will be a consideration. While U.S. TIPS are the most direct inflation protection for a U.S. portfolio, consideration of a global TIPS portfolio can provide duration flexibility to a TIPS program.

The following chart shows the correlation of these investments to inflation.

2022 capital market assumptions and outlooks

As we review new capital market assumptions for 2022, it’s interesting to note that we are seeing those assumptions include a higher inflation rate. That will, in turn, flow through to our 2022 investment outlooks.

So, how should we be thinking about inflation? As previously stated, we believe that inflation, like all other portfolio risks, including interest rates and market risk, should be discussed as part of creating a well-diversified portfolio.

See more insights

U.S. Dollar Strength

Role of Q4 2022 Investment Performance in Rise of Model Pension Plan’s Funded Status

"2023: The Year of the Rabbit” Investment Outlook

The information and opinions herein provided by third parties have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed. This article and the data and analysis herein is intended for general education only and not as investment advice. It is not intended for use as a basis for investment decisions, nor should it be construed as advice designed to meet the needs of any particular investor. On all matters involving legal interpretations and regulatory issues, investors should consult legal counsel.