Articles | May 25, 2021

Top Five Reasons the U.S. Fed Will Keep Rates Low for Now

A major question facing investors relates to the actions of the U.S. Federal Reserve when it comes to short-term interest rates under their explicit control. Maintaining rates at the current low levels is indicative of their support for continued economic growth by suppressing the cost of borrowed capital.

Conversely, if the Fed were to begin to raise rates, this would signal a perspective that either the economy is running too fast and needs to be held in check or that we’re able to return to a more normal rate environment. While the Fed has signaled an intent to maintain its low rate stance, they always reserve the ability to change that position based upon actual economic variables as they occur. In this case, however, we believe there are a number of reasons to expect that the Fed’s guidance will in fact remain in place at least for the next 12 to 18 months barring some substantial changes in economic vitality in the U.S.

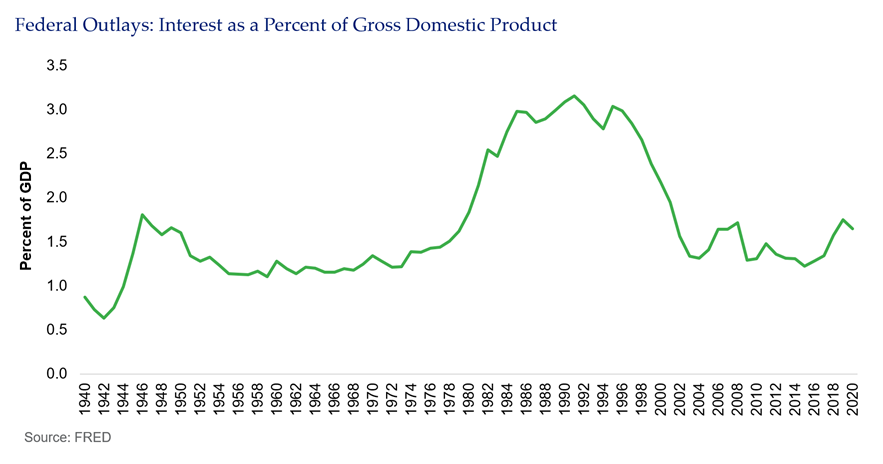

Reason #1: Debt Service

We’re all aware of the mountain of debt created by a combination of monetary and fiscal policy implemented by the U.S. Fed and government over the last decade plus. As reported, it’s now, even as a percentage of GDP, eclipsed what was outstanding while we were fighting and winning World War II. When we look at the key metric of how much of our GDP goes to servicing that debt, the number is actually pretty reasonable. A large part of that rosier picture is the result of the current low levels of interest paid by the Treasury on the outstanding debt. Imagine, if you will, that rates double in the short term and the cost of servicing skyrockets. The implications of higher debt service could result in crowding out other governmental spending that supports economic growth or increases the level of the debt burden as that can is kicked down the road.

Reason #2: Real yields

Historically, low global real yields have encouraged foreign savings and investment to flow into the U.S., the result of a flight to quality as well as the U.S. dollar remaining the world’s reserve currency. This also helps to keep U.S. rates low. Theoretically, these low real yields in the U.S. make it cheaper for U.S. companies to borrow and invest, (and recent issuance tells us they are borrowing), as well as supporting the value of stocks through a lower discount rate for future earnings. This time around, perceived higher inflation is compounding lower real rates. If inflation heats up to the extent that markets are pricing in, the Fed’s challenge will be to put the U.S. in a global sweet spot where yields and reserve currency status will attract foreign capital and investment, yet not be so low that the trend reverses itself and global savings moves away from our shores. We believe the Fed’s narrative of “transitory inflation” is relevant, as you will see in reasons #3 and #4 below. An increase in rates might spur greater foreign flows, but could choke off the desire to invest by U.S. companies, slowing the economy and hitting the equity markets with both fists (increased discount rates and lower economic growth).

Reason #3: Millions still out of the labor force

While there has been much fanfare about the dramatic recovery from jobs lost in the pandemic, at this writing there are still almost 4 million unemployed when compared to the pre-pandemic period. In addition, principally due to demographics, the level of stimulus and changing family dynamics, many potential workers appear to have left the labor force and may not return any time soon. The Fed realizes that the combination of an increasing labor force and productivity improvements are the bedrocks of stable economic growth. Low rates will encourage employers to invest in their businesses’ future, which should serve, particularly if labor markets tighten somewhat, to encourage many to return to work and develop more productive methods of delivering goods and services.

Reason #4: Wage growth has remained weak

This Fed, unlike many in the past, recognizes that the formula for success will also be driven by not just the magnitude of employment itself, but by the nature of that employment. To this point much of the recovery in terms of income and wealth has disproportionately rewarded the top 10 percent. Meanwhile, wage growth for many, as well as non-stimulus-created wealth, has remained stubbornly low especially for the bottom 50 percent. Wage growth within that segment of the population tends to lead to more sustainable spending patterns as the proportion of their income that goes to basic needs is substantially greater than for the top 10 percent. As noted above, lower rates will support continued economic growth which should result in a more favorable environment for wages overall and especially for the bottom half.

Reason #5: Overshoot better than the alternatives

The Fed’s inflation policy (known as Flexible Inflation Targeting or FIT) explicitly describes the acceptability of overshooting on inflation, particularly given the long period of undershooting versus the 2 percent target. The Fed also has a great deal of flexibility as to how they measure their goals going forward, making it much easier to hit a target that can move as deemed appropriate. The Fed understands that in this time of historically low rates, an undershoot of growth leaves few options for economic stimulus, while conversely it provides a great deal of room to tap on the brakes if the engine starts pushing it all too fast. Although we don’t want to place much significance on the political nature of the Fed’s responsibilities, there is no doubt that it would be easier to explain an economy that is too hot over one that is too cold.

There is a delicate balance the Fed must achieve in providing stable and consistent guidance to market participants while being able to respond to changes in economic conditions as they occur. Clearly, as we come out of the pandemic, this balance is particularly challenging given this is an environment without recent precedent. Nonetheless, for the reasons stated above, and others, we expect the Fed will be motivated to stay the course with low rates and be quite reluctant to hit the panic button of monetary tightening. There is the possibility that the Fed’s approach to monetary policy may be tempered by even more rounds of fiscal stimulus. In that case, which seems to be on the table, they might decide to step back from very low rates while letting government spending bear more of the load of economic prosperity and equality. As always, the future is uncertain, but the implications of such action is an important consideration.

See related insights

The U.S. Fiscal Condition: “Another Day Older and Deeper in Debt”

What’s Driving a Steepening Yield Curve?

Cozy: The U.S. Economy in Three Graphs

The information and opinions herein provided by third parties have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed. This article and the data and analysis herein is intended for general education only and not as investment advice. It is not intended for use as a basis for investment decisions, nor should it be construed as advice designed to meet the needs of any particular investor. On all matters involving legal interpretations and regulatory issues, investors should consult legal counsel.